For decades, the Asian stainless steel supply chain resembled a well-choreographed dance, a classic iteration of the "flying geese" model where comparative advantage dictated a harmonious division of labor. Japan and South Korea provided capital and high-end technical expertise, China handled mid-tier manufacturing, and Southeast Asia served as the resource basket and downstream processor. That era of symbiotic cooperation is effectively over. In its place, a zero-sum battle for survival has emerged, precipitated by a deluge of capacity from China and Indonesia that has shattered the region’s trade equilibrium. What was once a model of industrial integration has devolved into a fractured landscape defined by "Red Sea" competition—a cutthroat environment where new trade barriers are rising rapidly as nations scramble to protect domestic industries from a tidal wave of low-cost metal.

The Low-Cost Deluge

The epicenter of this seismic shift lies in the aggressive industrial strategies of China and Indonesia, which are rapidly rewriting the region’s trade map. Indonesia’s transformation is particularly stark; moving beyond its traditional role as a raw material exporter, Jakarta has successfully leveraged its massive nickel reserves—and Chinese capital—to climb the value chain.

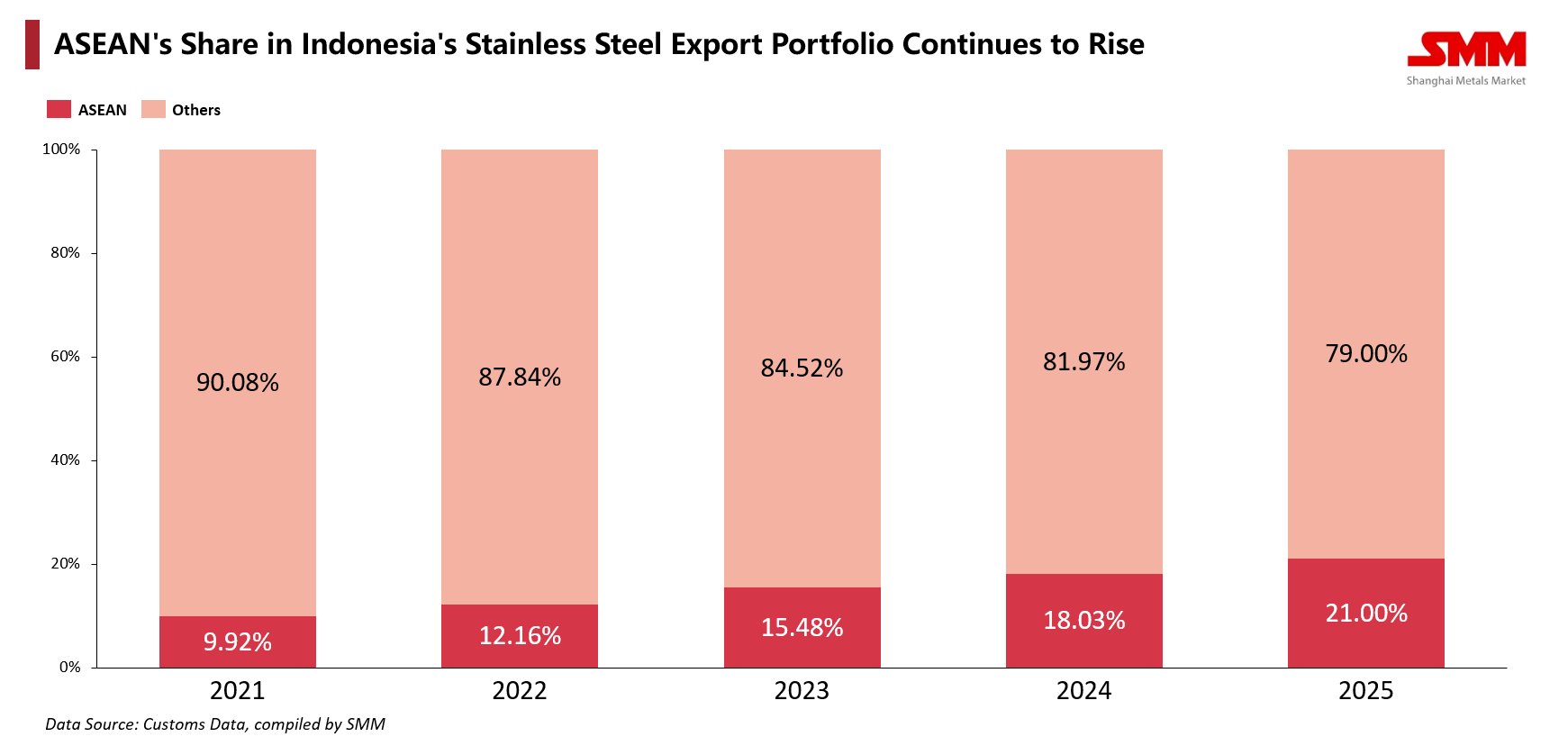

According to SMM statistics, Indonesian stainless steel exports surged to 3.43 million tons in the first three quarters of 2025, with shipments to its Southeast Asian neighbors jumping by 17.21%. More telling is the structural deepening of this dependence: Southeast Asia’s share of Indonesia’s export portfolio has more than doubled from 9.92% in 2021 to 21.00% in 2025. This is not merely trade; it is market capture. With exports to Thailand increasing by 28% and shipments to Malaysia soaring by a staggering 103%, Indonesia has graduated from a mineral supplier to a dominant manufacturer of finished and semi-finished goods, aggressively cannibalizing the market share previously held by established players.

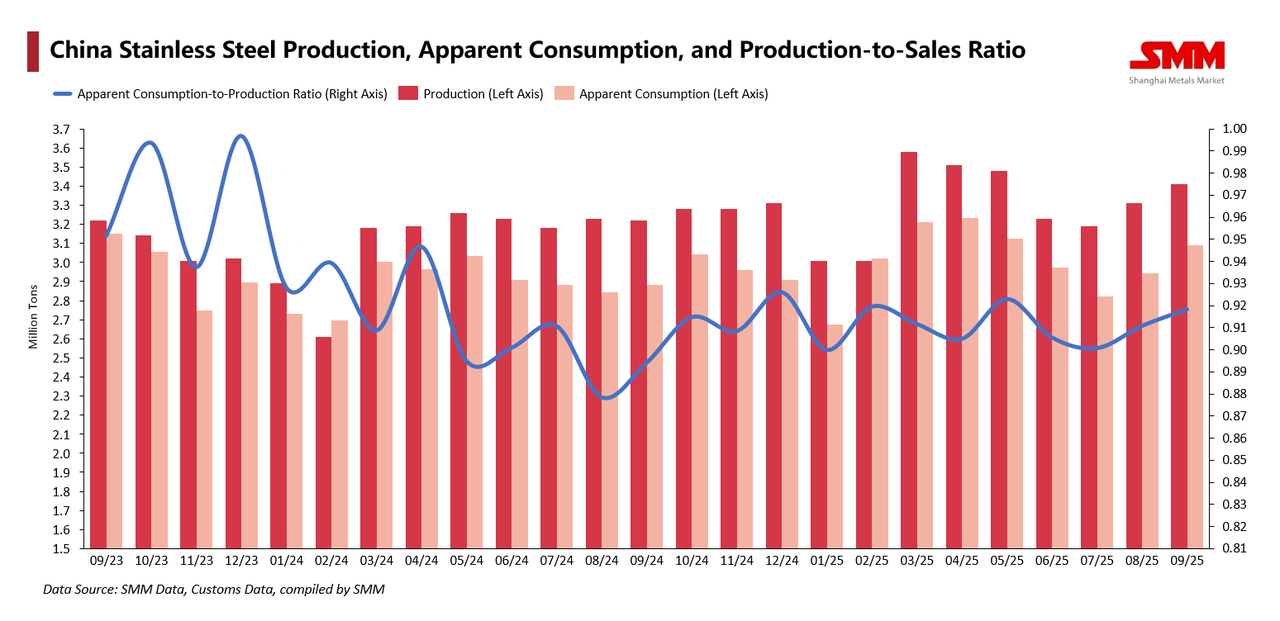

Simultaneously, China is grappling with its own internal imbalances, exporting its excess capacity as a deflationary force upon the region. Despite producing a colossal 33.19 million tons between January and October 2025—securing more than half the global total—China’s domestic engines of real estate and manufacturing are sputtering, leaving domestic consumption unable to absorb the output. SMM data indicates a declining domestic absorption rate, transforming export channels from an option into a lifeline. As traditional mature markets like South Korea and Taiwan saturate, Chinese steelmakers have aggressively pivoted toward India, Turkey, and the transshipment hub of Vietnam. The result is a crushing price war: in ASEAN ports, Chinese and Indonesian cold-rolled coils are frequently landing with CFR quotes hundreds of dollars per ton lower than their Japanese or South Korean equivalents. It is a discrepancy that transcends mere efficiency; for the high-cost incumbents, it represents a "dimensional strike" against their pricing power.

The Incumbents’ Retreat

The fallout has forced the region’s traditional industrial aristocrats, Japan and South Korea, into a retreat. Facing the dual pressure of the "China Price" and the "Indonesia Cost," their premium product strategies are faltering, leading to stagnant or shrinking footprints in key markets like Vietnam, Thailand, and Malaysia.

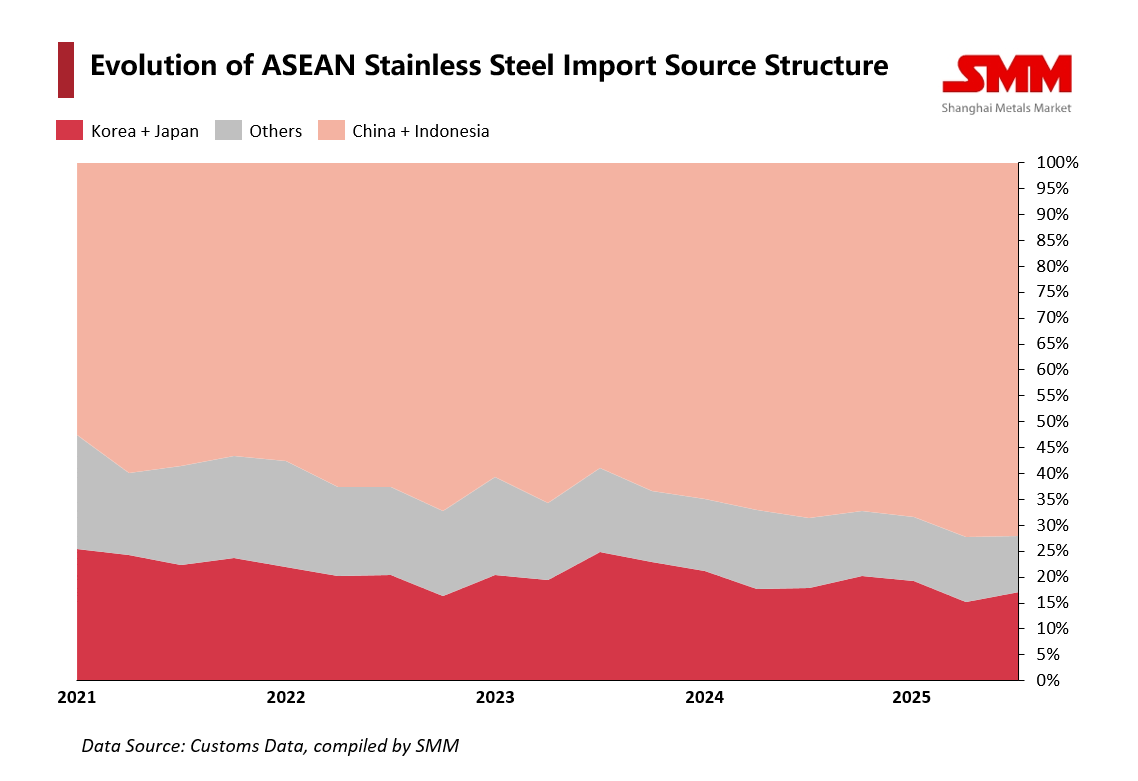

Import distribution charts clearly show the pink areas representing China and Indonesia squeezing out the red zones of Japanese and Korean share. This pressure is driving a strategic capitulation disguised as cooperation. A prime example is South Korea’s POSCO, which, acknowledging the futility of direct price competition, has opted for a pragmatic restructuring. In 2025, POSCO established a joint venture with China’s Tsingshan Group on Sulawesi Island, Indonesia, to build a plant with an annual capacity of 2 million tons, while simultaneously optimizing its assets within China. This move signals a profound shift from rivalry to "coopetition," where legacy producers are forced to integrate the cost advantages of China and Indonesia with their own technical heritage to survive.

The Protectionist Spiral

Where corporate strategy ends, political barriers begin. The region has entered a phase of "defensive realism," characterized by a domino effect of trade investigations and tariffs between 2024 and 2025. Japan, historically a stalwart of free trade, broke its silence in July 2025 by launching unprecedented anti-dumping investigations into nickel-based cold-rolled products from China and Taiwan. It was a tacit admission that the Japanese steel sector could no longer withstand the import pressure without state intervention. South Korea has been even more aggressive, deploying a "double-counter" strategy: taxing Chinese coils in May 2024 and imposing emergency provisional anti-dumping duties on hot-rolled thick plates in early 2025. With imports now accounting for more than half of the Korean market, Seoul is attempting to lock in price commitments to defend its industrial base. Even within ASEAN, the fraternity has fractured; Thailand has launched investigations against Vietnam, and Malaysia is reviewing products from six neighboring countries.

A Fragmented Future

Yet, the response is not uniform. Vietnam offers a counter-narrative of calculated pragmatism. By lifting anti-dumping measures on cold-rolled stainless steel from multiple countries in 2024, Hanoi prioritized the needs of its booming downstream manufacturing sector over the protection of upstream steel producers. It is a reminder that in this chaotic restructuring, the interests of steel consumers and producers are increasingly misaligned. Ultimately, the Asian stainless steel market has transitioned from a vertically integrated ecosystem to a horizontal battlefield of attrition. While China and Indonesia remain on the offensive, friction exists even within the low-cost camp, evidenced by continued anti-dumping duties on billets between the two. With the structural imbalance of supply and demand unlikely to resolve shortly, the region faces a future of deepening segmentation: a fragmented market where high barriers protect legacy players, while low-cost heavyweights aggressively flood every remaining fissure. For the region's economies, stainless steel overcapacity is no longer just a diplomatic dispute with the West; it has metastasized into a structural domestic crisis.

Written by: Bruce Chew

![[SMM Analysis] Rigid Demand Remained Steady During the Peak March Season, Stainless Steel Inventory Edged Up Slightly While Destocking Pressure Persisted](https://imgqn.smm.cn/usercenter/TdoSs20251217171724.jpeg)

![[SMM Stainless Steel Daily Review] News-Driven Disturbances Pushed SS Futures Higher, While Confidence in the Stainless Steel Spot Market Gradually Recovered](https://imgqn.smm.cn/usercenter/UrrTG20251217171717.jpg)

![[SMM Stainless Steel Daily Review] SS Futures Fluctuated Higher, and Stainless Steel Spot Prices Followed the Upward Trend](https://imgqn.smm.cn/usercenter/JdqON20251217171718.png)